Karl Pearson was a British mathematician who as soon as mentioned “Statistics is the grammar of science”. This holds true particularly for Computer and Information Sciences, Physical Science, and Biological Science.

When you might be getting began together with your journey in Data Science, Data Analytics, Machine Learning, or AI (together with Generative AI) having statistical data will show you how to higher leverage knowledge insights and truly perceive all of the algorithms past their implementation strategy.

I can not overstate the significance of statistics in knowledge science and Artificial Intelligence. Statistics supplies instruments and strategies to search out construction and provides deeper knowledge insights. Both Statistics and Mathematics love details and hate guesses. Knowing the basics of those two vital topics will assist you to assume critically, and be inventive when utilizing the info to unravel enterprise issues and make data-driven selections.

Key statistical ideas in your knowledge science or knowledge evaluation journey with Python Code

In this handbook, I’ll cowl the next Statistics matters for knowledge science, machine studying, and synthetic intelligence (together with GenAI):

If you haven’t any prior Statistical data and also you need to establish and study the important statistical ideas from the scratch and put together in your job interviews, then this handbook is for you. It can even be a great learn for anybody who desires to refresh their statistical data.

Prerequisites

Before you begin studying this handbook about key ideas in Statistics for Data Science, Machine Learning, and Artificial Intelligence, there are a couple of conditions that can show you how to take advantage of out of it.

This checklist is designed to make sure you are well-prepared and may totally grasp the statistical ideas mentioned:

- Basic Mathematical Skills: Comfort with highschool degree arithmetic, together with algebra and fundamental calculus, is crucial. These expertise are essential for understanding statistical formulation and strategies.

- Logical Thinking: Ability to assume logically and methodically to unravel issues will support in understanding statistical reasoning and making use of these ideas to data-driven eventualities.

- Computer Literacy: Basic data of utilizing computer systems and the web is important since many examples and workouts may require the usage of statistical software program or coding.

- Basic data of Python, such because the creation of variables and dealing with some fundamental knowledge buildings and coding can be required (if you’re not acquainted with these ideas, take a look at my Python for Data Science 2024 -Full Course for Beginners right here).

- Curiosity and Willingness to Learn: A eager curiosity in studying and exploring knowledge is probably crucial prerequisite. The subject of information science is consistently evolving, and a proactive strategy to studying might be extremely helpful.

This handbook assumes no prior data of statistics, making it accessible to novices. Still, familiarity with the above ideas will enormously improve your understanding and talent to use statistical strategies successfully in numerous domains.

If you need to study Mathematics, Statistics, Machine Learning or AI take a look at our YouTube Channel and LunarTech.ai without spending a dime sources.

Random Variables

Random variables kind the cornerstone of many statistical ideas. It may be arduous to digest the formal mathematical definition of a random variable, however merely put, it is a solution to map the outcomes of random processes, comparable to flipping a coin or rolling a cube, to numbers.

For occasion, we will outline the random strategy of flipping a coin by random variable X which takes a price 1 if the result is heads and 0 if the result is tails.

$$X =

start{circumstances}

1 & textual content{if heads}

0 & textual content{if tails}

finish{circumstances}

$$

In this instance, we now have a random strategy of flipping a coin the place this experiment can produce two attainable outcomes: {0,1}. This set of all attainable outcomes is named the pattern house of the experiment. Each time the random course of is repeated, it’s known as an occasion.

In this instance, flipping a coin and getting a tail as an end result is an occasion. The likelihood or the probability of this occasion occurring with a selected end result is named the likelihood of that occasion.

A likelihood of an occasion is the probability {that a} random variable takes a selected worth of x which may be described by P(x). In the instance of flipping a coin, the probability of getting heads or tails is identical, that’s 0.5 or 50%. So we now have the next setting:

$$Pr(X = textual content{heads}) = 0.5

Pr(X = textual content{tails}) = 0.5

$$

the place the likelihood of an occasion, on this instance, can solely take values within the vary [0,1].

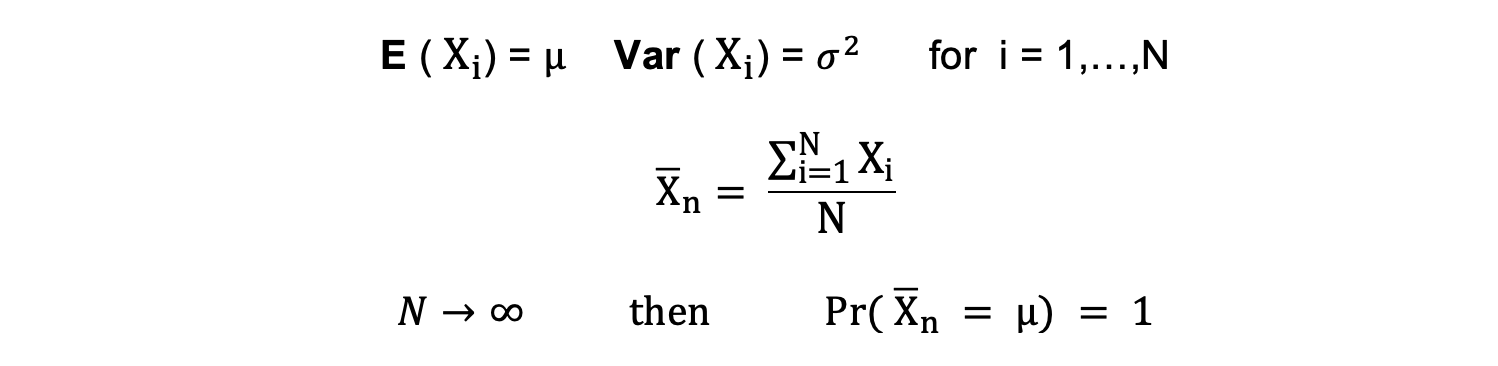

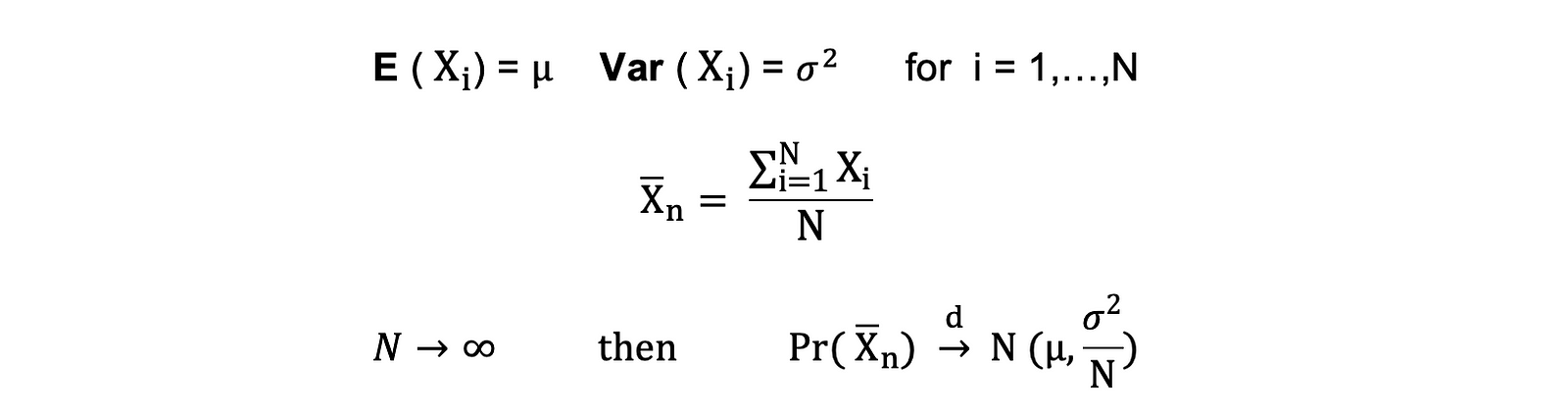

Mean, Variance, Standard Deviation

To perceive the ideas of imply, variance, and plenty of different statistical matters, it is very important study the ideas of inhabitants and pattern.

The inhabitants is the set of all observations (people, objects, occasions, or procedures) and is often very giant and various. On the opposite hand, a pattern is a subset of observations from the inhabitants that ideally is a real illustration of the inhabitants.

Given that experimenting with a whole inhabitants is both unattainable or just too costly, researchers or analysts use samples relatively than the whole inhabitants of their experiments or trials.

To make it possible for the experimental outcomes are dependable and maintain for the whole inhabitants, the pattern must be a real illustration of the inhabitants. That is, the pattern must be unbiased.

For this goal, we will use statistical sampling strategies comparable to Random Sampling, Systematic Sampling, Clustered Sampling, Weighted Sampling, and Stratified Sampling.

Mean

The imply, also referred to as the common, is a central worth of a finite set of numbers. Let’s assume a random variable X within the knowledge has the next values:

$$ X_1, X_2, X_3, ldots, X_N $$

the place N is the variety of observations or knowledge factors within the pattern set or just the info frequency. Then the pattern imply outlined by μ, which could be very typically used to approximate the inhabitants imply, may be expressed as follows:

$$

mu = frac{sum_{i=1}^{N} x_i}{N}

$$

The imply can be known as expectation which is commonly outlined by E() or random variable with a bar on the highest. For instance, the expectation of random variables X and Y, that’s E(X) and E(Y), respectively, may be expressed as follows:

$$

bar{X} = frac{sum_{i=1}^{N} X_i}{N}

$$

$$

bar{Y} = frac{sum_{i=1}^{N} Y_i}{N}

$$

Now that we now have a stable understanding of the imply as a statistical measure, let’s have a look at how we will apply this information virtually utilizing Python. Python is a flexible programming language that, with the assistance of libraries like NumPy, makes it straightforward to carry out complicated mathematical operations—together with calculating the imply.

In the next code snippet, we exhibit easy methods to compute the imply of a set of numbers utilizing NumPy. We will begin by exhibiting the calculation for a easy array of numbers. Then, we’ll deal with a typical situation encountered in knowledge science: calculating the imply of a dataset that features undefined or lacking values, represented as NaN (Not a Number). NumPy supplies a operate particularly designed to deal with such circumstances, permitting us to compute the imply whereas ignoring these NaN values.

Here is how one can carry out these operations in Python:

import numpy as np

import math

x = np.array([1,3,5,6])

mean_x = np.imply(x)

# in case the info incorporates Nan values

x_nan = np.array([1,3,5,6, math.nan])

mean_x_nan = np.nanmean(x_nan)Variance

The variance measures how far the info factors are unfold out from the common worth. It’s equal to the sum of the squares of the variations between the info values and the common (the imply).

We can categorical the inhabitants variance as follows:

x = np.array([1,3,5,6])

variance_x = np.var(x)

# right here that you must specify the levels of freedom (df) max variety of logically unbiased knowledge factors which have freedom to range

x_nan = np.array([1,3,5,6, math.nan])

mean_x_nan = np.nanvar(x_nan, ddof = 1)For deriving expectations and variances of various common likelihood distribution features, take a look at this Github repo.

Standard Deviation

The customary deviation is just the sq. root of the variance and measures the extent to which knowledge varies from its imply. The customary deviation outlined by sigma may be expressed as follows:

$$

sigma^2 = frac{sum_{i=1}^{N} (x_i – mu)^2}{N}

$$

Standard deviation is commonly most well-liked over the variance as a result of it has the identical models as the info factors, which suggests you’ll be able to interpret it extra simply.

To compute the inhabitants variance utilizing Python, we make the most of the var operate from the NumPy library. By default, this operate calculates the inhabitants variance by setting the ddof (Delta Degrees of Freedom) parameter to 0. However, when coping with samples and never the whole inhabitants, you’d usually set ddof to 1 to get the pattern variance.

The code snippet supplied exhibits easy methods to calculate the variance for a set of information. Additionally, it exhibits easy methods to calculate the variance when there are NaN values within the knowledge. NaN values symbolize lacking or undefined knowledge. When calculating the variance, these NaN values have to be dealt with appropriately; in any other case, they may end up in a variance that isn’t a quantity (NaN), which is uninformative.

Here is how one can calculate the inhabitants variance in Python, taking into consideration the potential presence of NaN values:

x = np.array([1,3,5,6])

variance_x = np.std(x)

x_nan = np.array([1,3,5,6, math.nan])

mean_x_nan = np.nanstd(x_nan, ddof = 1)Covariance

The covariance is a measure of the joint variability of two random variables and describes the connection between these two variables. It is outlined because the anticipated worth of the product of the 2 random variables’ deviations from their means.

The covariance between two random variables X and Z may be described by the next expression, the place E(X) and E(Z) symbolize the technique of X and Z, respectively.

$$textual content{Cov}(X, Z) = Eleft[(X – E(X))(Z – E(Z))right]$$

Covariance can take adverse or constructive values in addition to a price of 0. A constructive worth of covariance signifies that two random variables are likely to range in the identical course, whereas a adverse worth means that these variables range in reverse instructions. Finally, the worth 0 signifies that they don’t range collectively.

To discover the idea of covariance virtually, we’ll use Python with the NumPy library, which supplies highly effective numerical operations. The np.cov operate can be utilized to calculate the covariance matrix for 2 or extra datasets. In the matrix, the diagonal components symbolize the variance of every dataset, and the off-diagonal components symbolize the covariance between every pair of datasets.

Let’s have a look at an instance of calculating the covariance between two units of information:

x = np.array([1,3,5,6])

y = np.array([-2,-4,-5,-6])

#this can return the covariance matrix of x,y containing x_variance, y_variance on diagonal components and covariance of x,y

cov_xy = np.cov(x,y)Correlation

The correlation can be a measure of a relationship. It measures each the energy and the course of the linear relationship between two variables.

If a correlation is detected, then it means that there’s a relationship or a sample between the values of two goal variables. Correlation between two random variables X and Z is the same as the covariance between these two variables divided by the product of the usual deviations of those variables. This may be described by the next expression:

$$rho_{X,Z} = frac{textual content{Cov}(X, Z)}{sigma_X sigma_Z}$$

Correlation coefficients’ values vary between -1 and 1. Keep in thoughts that the correlation of a variable with itself is all the time 1, that’s Cor(X, X) = 1.

Another factor to remember when decoding correlation is to not confuse it with causation, given {that a} correlation is just not essentially a causation. Even if there’s a correlation between two variables, you can’t conclude that one variable causes a change within the different. This relationship could possibly be coincidental, or a 3rd issue may be inflicting each variables to alter.

x = np.array([1,3,5,6])

y = np.array([-2,-4,-5,-6])

corr = np.corrcoef(x,y)

Probability Distribution Functions

A operate that describes all of the attainable values, the pattern house, and the corresponding chances {that a} random variable can take inside a given vary, bounded between the minimal and most attainable values, is named a likelihood distribution operate (pdf) or likelihood density.

Every pdf must fulfill the next two standards:

$$0 leq Pr(X) leq 1 \

sum p(X) = 1

$$

the place the primary criterium states that each one chances needs to be numbers within the vary of [0,1] and the second criterium states that the sum of all attainable chances needs to be equal to 1.

Probability features are often categorized into two classes: discrete and steady.

Discrete distribution operate describes the random course of with countable pattern house, like in an instance of tossing a coin that has solely two attainable outcomes. Continuous distribution features describe the random course of with a steady pattern house.

Examples of discrete distribution features are Bernoulli, Binomial, Poisson, Discrete Uniform. Examples of steady distribution features are Normal, Continuous Uniform, Cauchy.

Binomial Distribution

The binomial distribution is the discrete likelihood distribution of the variety of successes in a sequence of n unbiased experiments, every with the boolean-valued end result: success (with likelihood p) or failure (with likelihood q = 1 − p).

Let’s assume a random variable X follows a Binomial distribution, then the likelihood of observing okay successes in n unbiased trials may be expressed by the next likelihood density operate:

$$Pr(X = okay) = binom{n}{okay} p^okay q^{n-k}$$

The binomial distribution is beneficial when analyzing the outcomes of repeated unbiased experiments, particularly in the event you’re within the likelihood of assembly a selected threshold given a selected error charge.

Binomial Distribution Mean and Variance

The imply of a binomial distribution, denoted as E(X)=np, tells you the common variety of successes you’ll be able to count on in the event you conduct n unbiased trials of a binary experiment.

A binary experiment is one the place there are solely two outcomes: success (with likelihood p) or failure (with likelihood q=1−p).

$$E(X) = np\

textual content{Var}(X) = npq

$$

For instance, in the event you have been to flip a coin 100 instances and also you outline successful because the coin touchdown on heads (as an instance the likelihood of heads is 0.5), the binomial distribution would let you know how seemingly it’s to get any variety of heads in these 100 flips. The imply E(X) could be 100×0.5=50, indicating that on common, you’d count on to get 50 heads.

The variance Var(X)=npq measures the unfold of the distribution, indicating how a lot the variety of successes is more likely to deviate from the imply.

Continuing with the coin flip instance, the variance could be 100×0.5×0.5=25, which informs you in regards to the variability of the outcomes. A smaller variance would imply the outcomes are extra tightly clustered across the imply, whereas a bigger variance signifies they’re extra unfold out.

These ideas are essential in lots of fields. For occasion:

- Quality Control: Manufacturers may use the binomial distribution to foretell the variety of faulty gadgets in a batch, serving to them perceive the standard and consistency of their manufacturing course of.

- Healthcare: In medication, it could possibly be used to calculate the likelihood of a sure variety of sufferers responding to a remedy, based mostly on previous success charges.

- Finance: In finance, binomial fashions are used to guage the danger of portfolio or funding methods by predicting the variety of instances an asset will attain a sure value level.

- Polling and Survey Analysis: When predicting election outcomes or buyer preferences, pollsters may use the binomial distribution to estimate how many individuals will favor a candidate or a product, given the likelihood drawn from a pattern.

Understanding the imply and variance of the binomial distribution is prime to decoding the outcomes and making knowledgeable selections based mostly on the probability of various outcomes.

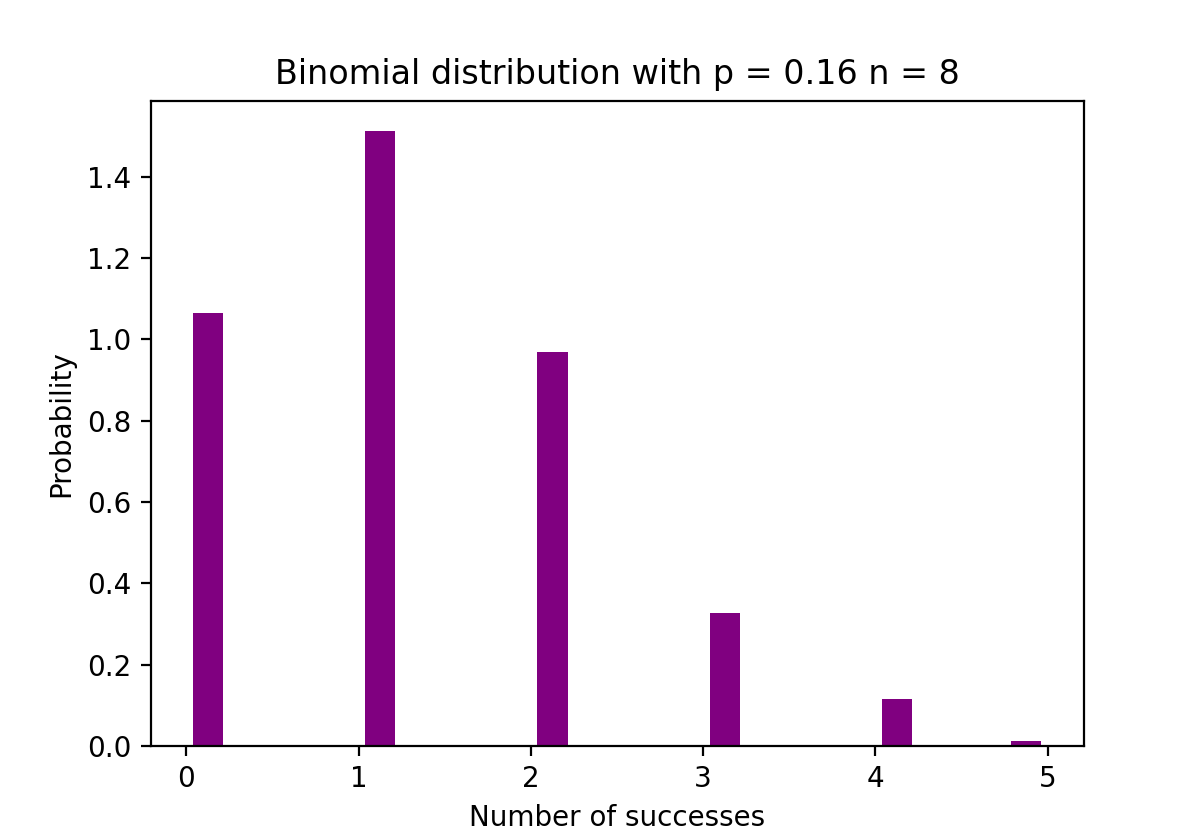

The determine beneath visualizes an instance of Binomial distribution the place the variety of unbiased trials is the same as 8 and the likelihood of success in every trial is the same as 16%.

The Python code beneath creates a histogram to visualise the distribution of outcomes from 1000 experiments, every consisting of 8 trials with successful likelihood of 0.16. It makes use of NumPy to generate the binomial distribution knowledge and Matplotlib to plot the histogram, exhibiting the likelihood of the variety of successes in these trials.

# Random Generation of 1000 unbiased Binomial samples

import numpy as np

import matplotlib.pyplot as plt

n = 8

p = 0.16

N = 1000

X = np.random.binomial(n,p,N)

# Histogram of Binomial distribution

counts, bins, ignored = plt.hist(X, 20, density = True, rwidth = 0.7, coloration="purple")

plt.title("Binomial distribution with p = 0.16 n = 8")

plt.xlabel("Number of successes")

plt.ylabel("Probability")plt.present()

Poisson Distribution

The Poisson distribution is the discrete likelihood distribution of the variety of occasions occurring in a specified time interval, given the common variety of instances the occasion happens over that point interval.

Let’s assume a random variable X follows a Poisson distribution. Then the likelihood of observing okay occasions over a time interval may be expressed by the next likelihood operate:

$$Pr(X = okay) = frac{lambda^okay e^{-lambda}}{okay!}

$$

the place e is Euler’s quantity and λ lambda, the arrival charge parameter, is the anticipated worth of X. The Poisson distribution operate could be very common for its utilization in modeling countable occasions occurring inside a given time interval.

Poisson Distribution Mean and Variance

The Poisson distribution is especially helpful for modeling the variety of instances an occasion happens inside a specified timeframe. The imply E(X) and variance Var(X)

Var(X) of a Poisson distribution are each equal to λ, which is the common charge at which occasions happen (also referred to as the speed parameter). This makes the Poisson distribution distinctive, as it’s characterised by this single parameter.

The proven fact that the imply and variance are equal signifies that as we observe extra occasions, the distribution of the variety of occurrences turns into extra predictable. It’s utilized in numerous fields comparable to enterprise, engineering, and science for duties like:

Predicting the variety of buyer arrivals at a retailer inside an hour. Estimating the variety of emails you’d obtain in a day. Understanding the variety of defects in a batch of supplies.

So, the Poisson distribution helps in making probabilistic forecasts in regards to the incidence of uncommon or random occasions over intervals of time or house.

$$E(X) = lambda\

textual content{Var}(X) = lambda

$$

For instance, Poisson distribution can be utilized to mannequin the variety of prospects arriving within the store between 7 and 10 pm, or the variety of sufferers arriving in an emergency room between 11 and 12 pm.

The determine beneath visualizes an instance of Poisson distribution the place we depend the variety of Web guests arriving on the web site the place the arrival charge, lambda, is assumed to be equal to 7 minutes.

In sensible knowledge evaluation, it’s typically useful to simulate the distribution of occasions. Below is a Python code snippet that demonstrates easy methods to generate a sequence of information factors that observe a Poisson distribution utilizing NumPy. We then create a histogram utilizing Matplotlib to visualise the distribution of the variety of guests (for instance) we would count on to see, based mostly on our common charge λ = 7

This histogram helps in understanding the distribution’s form and variability. The most certainly variety of guests is across the imply λ, however the distribution exhibits the likelihood of seeing fewer or higher numbers as nicely.

# Random Generation of 1000 unbiased Poisson samples

import numpy as np

lambda_ = 7

N = 1000

X = np.random.poisson(lambda_,N)

# Histogram of Poisson distribution

import matplotlib.pyplot as plt

counts, bins, ignored = plt.hist(X, 50, density = True, coloration="purple")

plt.title("Randomly producing from Poisson Distribution with lambda = 7")

plt.xlabel("Number of holiday makers")

plt.ylabel("Probability")

plt.present()Normal Distribution

The Normal likelihood distribution is the continual likelihood distribution for a real-valued random variable. Normal distribution, additionally known as Gaussian distribution is arguably some of the common distribution features that’s generally utilized in social and pure sciences for modeling functions. For instance, it’s used to mannequin folks’s top or check scores.

Let’s assume a random variable X follows a Normal distribution. Then its likelihood density operate may be expressed as follows:

$$Pr(X = okay) = frac{1}{sigmasqrt{2pi}} e^{-frac{1}{2} left(frac{x-mu}{sigma}proper)^2}

$$

the place the parameter μ (mu) is the imply of the distribution additionally known as the location parameter, parameter σ (sigma) is the usual deviation of the distribution additionally known as the scale parameter. The quantity π (pi) is a mathematical fixed roughly equal to three.14.

Normal Distribution Mean and Variance

$$E(X) = mu\

textual content{Var}(X) = sigma^2$$

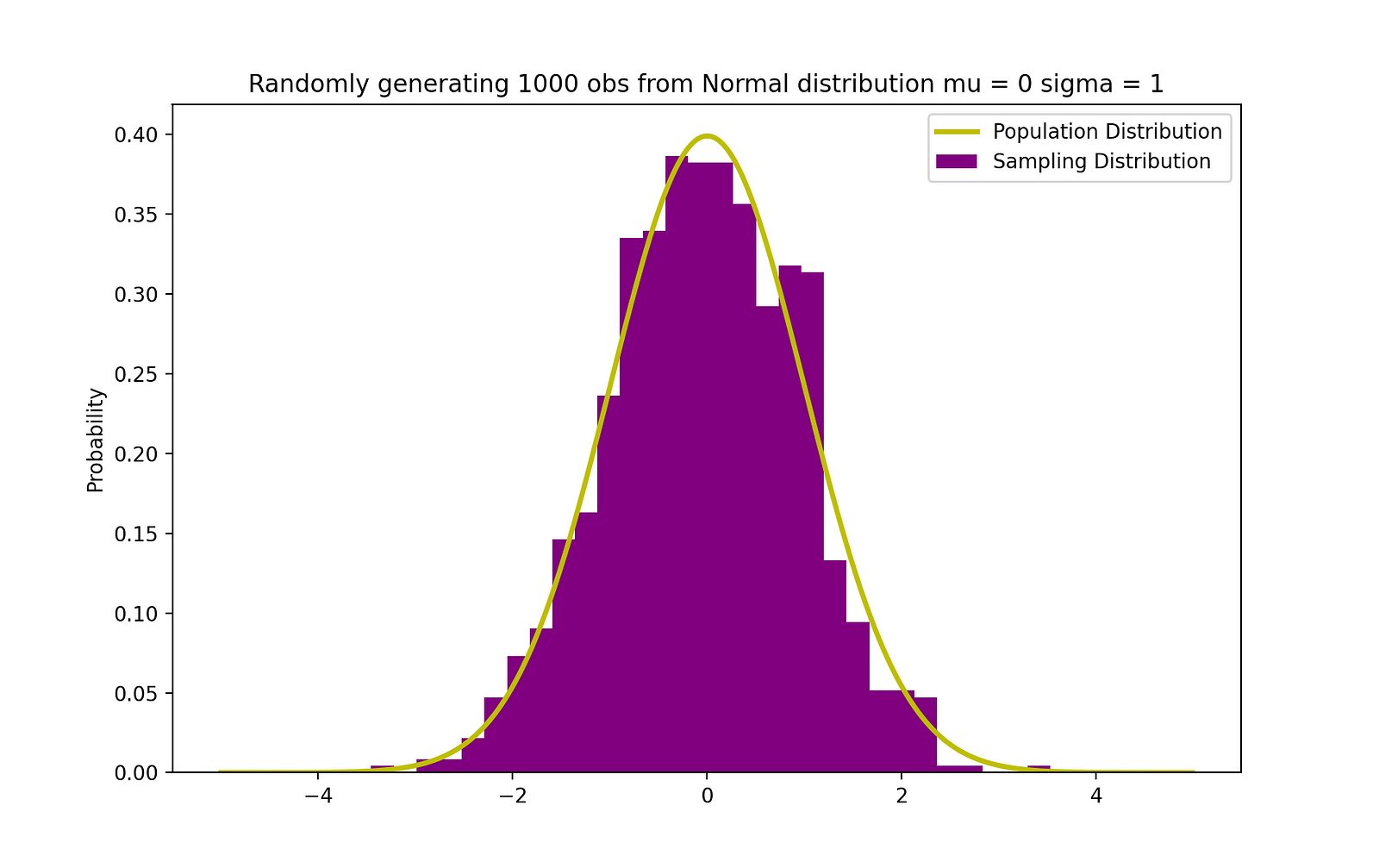

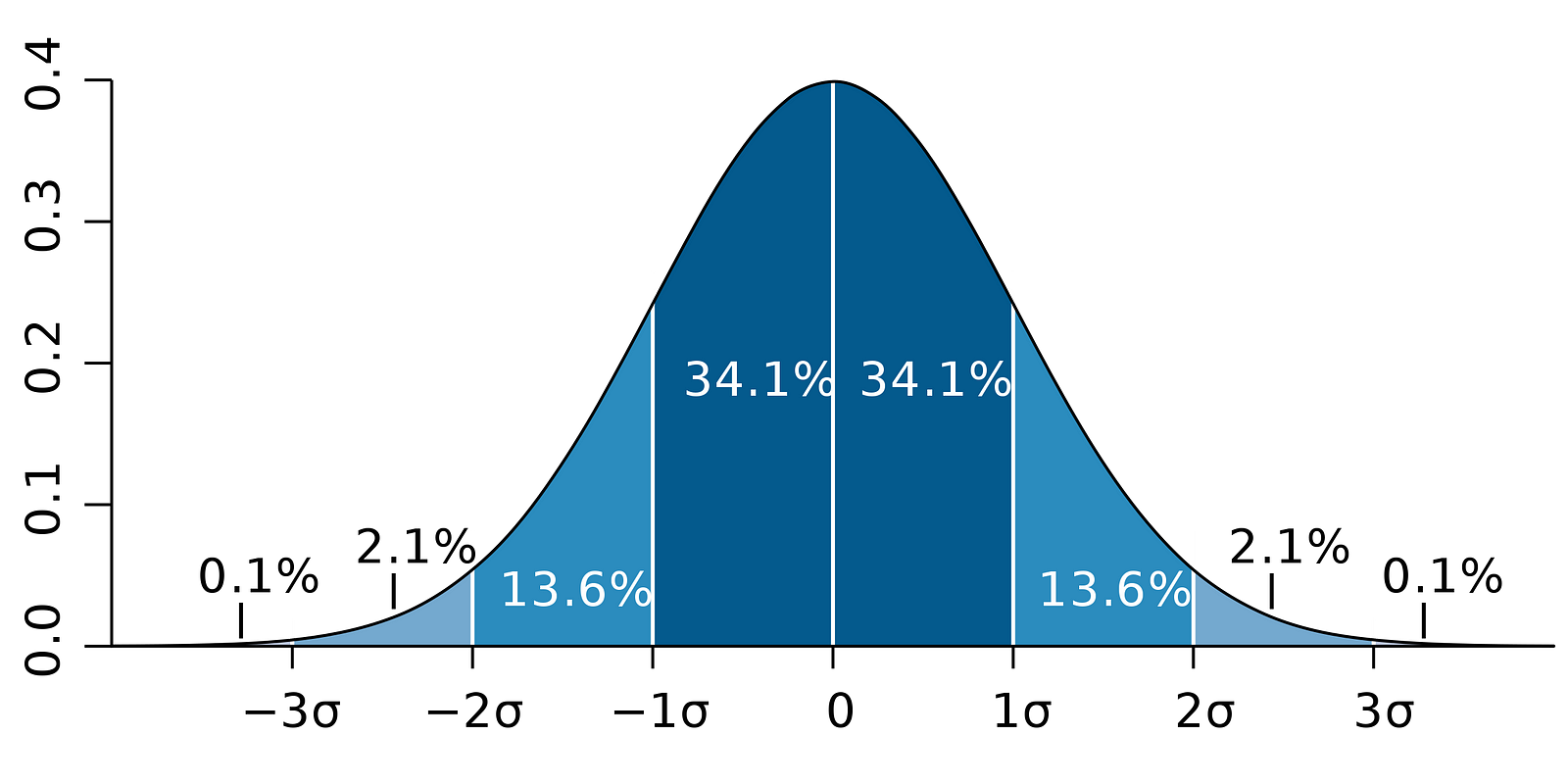

The determine beneath visualizes an instance of Normal distribution with a imply 0 (μ = 0) and customary deviation of 1 (σ = 1), which is known as Standard Normal distribution which is symmetric.

The visualization of the usual regular distribution is essential as a result of this distribution underpins many statistical strategies and likelihood principle. When knowledge is generally distributed with a imply ( μ ) of 0 and customary deviation (σ) of 1, it’s known as the usual regular distribution. It’s symmetric across the imply, with the form of the curve typically known as the “bell curve” on account of its bell-like form.

The customary regular distribution is prime for the next causes:

- Central Limit Theorem: This theorem states that, below sure circumstances, the sum of a lot of random variables might be roughly usually distributed. It permits for the usage of regular likelihood principle for pattern means and sums, even when the unique knowledge is just not usually distributed.

- Z-Scores: Values from any regular distribution may be reworked into the usual regular distribution utilizing Z-scores, which point out what number of customary deviations a component is from the imply. This permits for the comparability of scores from completely different regular distributions.

- Statistical Inference and AB Testing: Many statistical checks, comparable to t-tests and ANOVAs, assume that the info follows a traditional distribution, or they depend on the central restrict theorem. Understanding the usual regular distribution helps within the interpretation of those checks’ outcomes.

- Confidence Intervals and Hypothesis Testing: The properties of the usual regular distribution are used to assemble confidence intervals and to carry out speculation testing.

All matters which we’ll cowl beneath!

So, with the ability to visualize and perceive the usual regular distribution is vital to making use of many statistical strategies precisely.

The Python code beneath makes use of NumPy to generate 1000 random samples from a traditional distribution with a imply (μ) of 0 and a normal deviation (σ) of 1, that are customary parameters for the usual regular distribution. These generated samples are saved within the variable X.

To visualize the distribution of those samples, the code employs Matplotlib to create a histogram. The plt.hist operate is used to plot the histogram of the samples with 30 bins, and the density parameter is about to True to normalize the histogram in order that the realm below it sums to 1. This successfully turns the histogram right into a likelihood density plot.

Additionally, the SciPy library is used to overlay the likelihood density operate (PDF) of the theoretical regular distribution on the histogram. The norm.pdf operate generates the y-values for the PDF given an array of x-values. This theoretical curve is plotted in yellow over the histogram to indicate how carefully the random samples match the anticipated distribution.

The ensuing graph shows the histogram of the generated samples in purple, with the theoretical regular distribution overlaid in yellow. The x-axis represents the vary of values that the samples can take, whereas the y-axis represents the likelihood density. This visualization is a strong instrument for evaluating the empirical distribution of the info with the theoretical mannequin, permitting us to see whether or not our samples observe the anticipated sample of a traditional distribution.

# Random Generation of 1000 unbiased Normal samples

import numpy as np

mu = 0

sigma = 1

N = 1000

X = np.random.regular(mu,sigma,N)

# Population distribution

from scipy.stats import norm

x_values = np.arange(-5,5,0.01)

y_values = norm.pdf(x_values)

#Sample histogram with Population distribution

import matplotlib.pyplot as plt

counts, bins, ignored = plt.hist(X, 30, density = True,coloration="purple",label="Sampling Distribution")

plt.plot(x_values,y_values, coloration="y",linewidth = 2.5,label="Population Distribution")

plt.title("Randomly producing 1000 obs from Normal distribution mu = 0 sigma = 1")

plt.ylabel("Probability")

plt.legend()

plt.present()

Bayes’ Theorem

The Bayes’ Theorem (typically known as Bayes’ Law) is arguably essentially the most highly effective rule of likelihood and statistics. It was named after well-known English statistician and thinker, Thomas Bayes.

Bayes’ theorem is a strong likelihood legislation that brings the idea of subjectivity into the world of Statistics and Mathematics the place every part is about details. It describes the likelihood of an occasion, based mostly on the prior info of circumstances that may be associated to that occasion.

For occasion, if the danger of getting Coronavirus or Covid-19 is thought to extend with age, then Bayes’ Theorem permits the danger to a person of a recognized age to be decided extra precisely. It does this by conditioning it on the age relatively than merely assuming that this particular person is frequent to the inhabitants as an entire.

The idea of conditional likelihood, which performs a central position in Bayes’ theorem, is a measure of the likelihood of an occasion taking place, on condition that one other occasion has already occurred.

Bayes’ theorem may be described by the next expression the place the X and Y stand for occasions X and Y, respectively:

$$Pr(X | Y) = frac X) Pr(X){Pr(Y)}

$$

- Pr (X|Y): the likelihood of occasion X occurring on condition that occasion or situation Y has occurred or is true

- Pr (Y|X): the likelihood of occasion Y occurring on condition that occasion or situation X has occurred or is true

- Pr (X) & Pr (Y): the chances of observing occasions X and Y, respectively

In the case of the sooner instance, the likelihood of getting Coronavirus (occasion X) conditional on being at a sure age is Pr (X|Y). This is the same as the likelihood of being at a sure age on condition that the particular person acquired a Coronavirus, Pr (Y|X), multiplied with the likelihood of getting a Coronavirus, Pr (X), divided by the likelihood of being at a sure age, Pr (Y).

Linear Regression

Earlier, we launched the idea of causation between variables, which occurs when a variable has a direct affect on one other variable.

When the connection between two variables is linear, then Linear Regression is a statistical methodology that may assist mannequin the affect of a unit change in a variable, the unbiased variable on the values of one other variable, the dependent variable.

Dependent variables are also known as response variables or defined variables, whereas unbiased variables are also known as regressors or explanatory variables.

When the Linear Regression mannequin relies on a single unbiased variable, then the mannequin is named Simple Linear Regression. When the mannequin relies on a number of unbiased variables, it’s known as Multiple Linear Regression.

Simple Linear Regression may be described by the next expression:

$$Y_i = beta_0 + beta_1X_i + u_i

$$

the place Y is the dependent variable, X is the unbiased variable which is a part of the info, β0 is the intercept which is unknown and fixed, β1 is the slope coefficient or a parameter similar to the variable X which is unknown and fixed as nicely. Finally, u is the error time period that the mannequin makes when estimating the Y values.

The fundamental thought behind linear regression is to search out the best-fitting straight line, the regression line, by way of a set of paired ( X, Y ) knowledge.

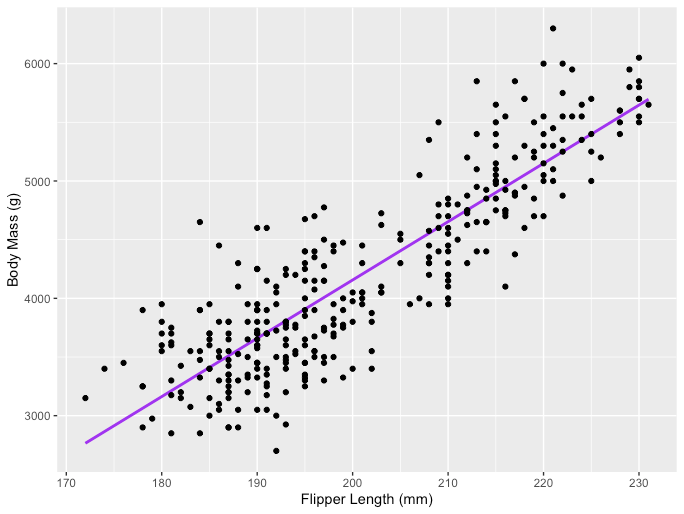

One instance of the Linear Regression utility is modeling the affect of flipper size on penguins’ physique mass, which is visualized beneath:

The R code snippet you’ve got shared is for making a scatter plot with a linear regression line utilizing the ggplot2 bundle in R, which is a strong and widely-used library for creating graphics and visualizations. The code makes use of a dataset named penguins from the palmerpenguins bundle, presumably containing knowledge about penguin species, together with measurements like flipper size and physique mass.

# R code for the graph

set up.packages("ggplot2")

set up.packages("palmerpenguins")

library(palmerpenguins)

library(ggplot2)

View(knowledge(penguins))

ggplot(knowledge = penguins, aes(x = flipper_length_mm,y = body_mass_g))+

geom_smooth(methodology = "lm", se = FALSE, coloration="purple")+

geom_point()+

labs(x="Flipper Length (mm)",y="Body Mass (g)")Multiple Linear Regression with three unbiased variables may be described by the next expression:

$$Y_i = beta_0 + beta_1X_{1,i} + beta_2X_{2,i} + beta_3X_{3,i} + u_i

$$

Ordinary Least Squares

The atypical least squares (OLS) is a technique for estimating the unknown parameters comparable to β0 and β1 in a linear regression mannequin. The mannequin relies on the precept of least squares. This minimizes the sum of the squares of the variations between the noticed dependent variable and its values which can be predicted by the linear operate of the unbiased variable (also known as fitted values).

This distinction between the true and predicted values of dependent variable Y is known as residual. So OLS minimizes the sum of squared residuals.

This optimization drawback leads to the next OLS estimates for the unknown parameters β0 and β1 that are also referred to as coefficient estimates:

$$hat{beta}_1 = frac{sum_{i=1}^{N} (X_i – bar{X})(Y_i – bar{Y})}{sum_{i=1}^{N} (X_i – bar{X})^2}$$

$$hat{beta}_0 = bar{Y} – hat{beta}_1bar{X}$$

Once these parameters of the Simple Linear Regression mannequin are estimated, the fitted values of the response variable may be computed as follows:

$$ hat{Y}_i = hat{beta}_0 + hat{beta}_1X_i $$

Standard Error

The residuals or the estimated error phrases may be decided as follows:

$$hat{u}_i = Y_i – hat{Y}_i$$

It is vital to remember the distinction between the error phrases and residuals. Error phrases are by no means noticed, whereas the residuals are calculated from the info. The OLS estimates the error phrases for every remark however not the precise error time period. So, the true error variance remains to be unknown.

Also, these estimates are topic to sampling uncertainty. This means that we are going to by no means have the ability to decide the precise estimate, the true worth, of those parameters from pattern knowledge in an empirical utility. But we will estimate it by calculating the pattern residual variance through the use of the residuals as follows:

$$hat{sigma}^2 = frac{sum_{i=1}^{N} hat{u}_i^2}{N – 2}

$$

This estimate for the variance of pattern residuals helps us estimate the variance of the estimated parameters, which is commonly expressed as follows:

$$textual content{Var}(hat{beta})

$$

The sq. root of this variance time period is named the usual error of the estimate. This is a key element in assessing the accuracy of the parameter estimates. It is used to calculate check statistics and confidence intervals.

The customary error may be expressed as follows:

$$SE(hat{beta}) = sqrt{textual content{Var}(hat{beta})}

$$

It is vital to remember the distinction between the error phrases and residuals. Error phrases are by no means noticed, whereas the residuals are calculated from the info.

OLS Assumptions

The OLS estimation methodology makes the next assumptions which must be glad to get dependable prediction outcomes:

- The Linearity assumption states that the mannequin is linear in parameters.

- The Random Sample assumption states that each one observations within the pattern are randomly chosen.

- The Exogeneity assumption states that unbiased variables are uncorrelated with the error phrases.

- The Homoskedasticity assumption states that the variance of all error phrases is fixed.

- The No Perfect Multi-Collinearity assumption states that not one of the unbiased variables is fixed and there aren’t any actual linear relationships between the unbiased variables.

The Python code snippet you’ve got shared performs Ordinary Least Squares (OLS) regression, which is a technique utilized in statistics to estimate the connection between unbiased variables and a dependent variable. This course of entails calculating the best-fit line by way of the info factors that minimizes the sum of the squared variations between the noticed values and the values predicted by the mannequin.

The code defines a operate runOLS(Y, X) that takes in a dependent variable Y and an unbiased variable X and performs the next steps:

- Estimates the OLS coefficients (beta_hat) utilizing the linear algebra answer to the least squares drawback.

- Makes predictions (

Y_hat) utilizing the estimated coefficients and calculates the residuals. - Computes the residual sum of squares (RSS), complete sum of squares (TSS), imply squared error (MSE), root imply squared error (RMSE), and R-squared worth, that are frequent metrics used to evaluate the match of the mannequin.

- Calculates the usual error of the coefficient estimates, t-statistics, p-values, and confidence intervals for the estimated coefficients.

These calculations are customary in regression evaluation and are used to interpret and perceive the energy and significance of the connection between the variables. The results of this operate contains the estimated coefficients and numerous statistics that assist consider the mannequin’s efficiency.

def runOLS(Y,X):

# OLS esyimation Y = Xb + e --> beta_hat = (X'X)^-1(X'Y)

beta_hat = np.dot(np.linalg.inv(np.dot(np.transpose(X), X)), np.dot(np.transpose(X), Y))

# OLS prediction

Y_hat = np.dot(X,beta_hat)

residuals = Y-Y_hat

RSS = np.sum(np.sq.(residuals))

sigma_squared_hat = RSS/(N-2)

TSS = np.sum(np.sq.(Y-np.repeat(Y.imply(),len(Y))))

MSE = sigma_squared_hat

RMSE = np.sqrt(MSE)

R_squared = (TSS-RSS)/TSS

# Standard error of estimates:sq. root of estimate's variance

var_beta_hat = np.linalg.inv(np.dot(np.transpose(X),X))*sigma_squared_hat

SE = []

t_stats = []

p_values = []

CI_s = []

for i in vary(len(beta)):

#customary errors

SE_i = np.sqrt(var_beta_hat[i,i])

SE.append(np.spherical(SE_i,3))

#t-statistics

t_stat = np.spherical(beta_hat[i,0]/SE_i,3)

t_stats.append(t_stat)

#p-value of t-stat p[|t_stat| >= t-treshhold two sided]

p_value = t.sf(np.abs(t_stat),N-2) * 2

p_values.append(np.spherical(p_value,3))

#Confidence intervals = beta_hat -+ margin_of_error

t_critical = t.ppf(q =1-0.05/2, df = N-2)

margin_of_error = t_critical*SE_i

CI = [np.round(beta_hat[i,0]-margin_of_error,3), np.spherical(beta_hat[i,0]+margin_of_error,3)]

CI_s.append(CI)

return(beta_hat, SE, t_stats, p_values,CI_s,

MSE, RMSE, R_squared)Parameter Properties

Under the belief that the OLS standards/assumptions we simply mentioned are glad, the OLS estimators of coefficients β0 and β1 are BLUE and Consistent. So what does this imply?

Gauss-Markov Theorem

This theorem highlights the properties of OLS estimates the place the time period BLUE stands for Best Linear Unbiased Estimator. Let’s discover what this implies in additional element.

Bias

The bias of an estimator is the distinction between its anticipated worth and the true worth of the parameter being estimated. It may be expressed as follows:

$$textual content{Bias}(beta, hat{beta}) = E(hat{beta}) – beta

$$

When we state that the estimator is unbiased, we imply that the bias is the same as zero. This implies that the anticipated worth of the estimator is the same as the true parameter worth, that’s:

$$E(hat{beta}) = beta$$

Unbiasedness doesn’t assure that the obtained estimate with any explicit pattern is equal or near β. What it means is that, if we repeatedly draw random samples from the inhabitants after which computes the estimate every time, then the common of those estimates could be equal or very near β.

Efficiency

The time period Best within the Gauss-Markov theorem pertains to the variance of the estimator and is known as effectivity. A parameter can have a number of estimators however the one with the bottom variance is named environment friendly.

Consistency

The time period consistency goes hand in hand with the phrases pattern dimension and convergence. If the estimator converges to the true parameter because the pattern dimension turns into very giant, then this estimator is claimed to be constant, that’s:

$$N to infty textual content{ then } hat{beta} to beta

$$

All these properties maintain for OLS estimates as summarized within the Gauss-Markov theorem. In different phrases, OLS estimates have the smallest variance, they’re unbiased, linear in parameters, and are constant. These properties may be mathematically confirmed through the use of the OLS assumptions made earlier.

Confidence Intervals

The Confidence Interval is the vary that incorporates the true inhabitants parameter with a sure pre-specified likelihood. This is known as the confidence degree of the experiment, and it is obtained through the use of the pattern outcomes and the margin of error.

Margin of Error

The margin of error is the distinction between the pattern outcomes and based mostly on what the consequence would have been in the event you had used the whole inhabitants.

Confidence Level

The Confidence Level describes the extent of certainty within the experimental outcomes. For instance, a 95% confidence degree signifies that in the event you have been to carry out the identical experiment repeatedly 100 instances, then 95 of these 100 trials would result in related outcomes.

Note that the boldness degree is outlined earlier than the beginning of the experiment as a result of it’s going to have an effect on how massive the margin of error might be on the finish of the experiment.

Confidence Interval for OLS Estimates

As I discussed earlier, the OLS estimates of the Simple Linear Regression, the estimates for intercept β0 and slope coefficient β1, are topic to sampling uncertainty. But we will assemble Confidence Intervals (CIs) for these parameters which is able to include the true worth of those parameters in 95% of all samples.

That is, 95% confidence interval for β may be interpreted as follows:

- The confidence interval is the set of values for which a speculation check can’t be rejected to the extent of 5%.

- The confidence interval has a 95% likelihood to include the true worth of β.

95% confidence interval of OLS estimates may be constructed as follows:

$$CI_{0.95}^{beta} = left[hat{beta}_i – 1.96 , SE(hat{beta}_i), hat{beta}_i + 1.96 , SE(hat{beta}_i)right]

$$

This relies on the parameter estimate, the usual error of that estimate, and the worth 1.96 representing the margin of error similar to the 5% rejection rule.

This worth is decided utilizing the Normal Distribution desk, which we’ll focus on in a while on this handbook.

Meanwhile, the next determine illustrates the concept of 95% CI:

Note that the boldness interval is dependent upon the pattern dimension as nicely, on condition that it’s calculated utilizing the usual error which relies on pattern dimension.

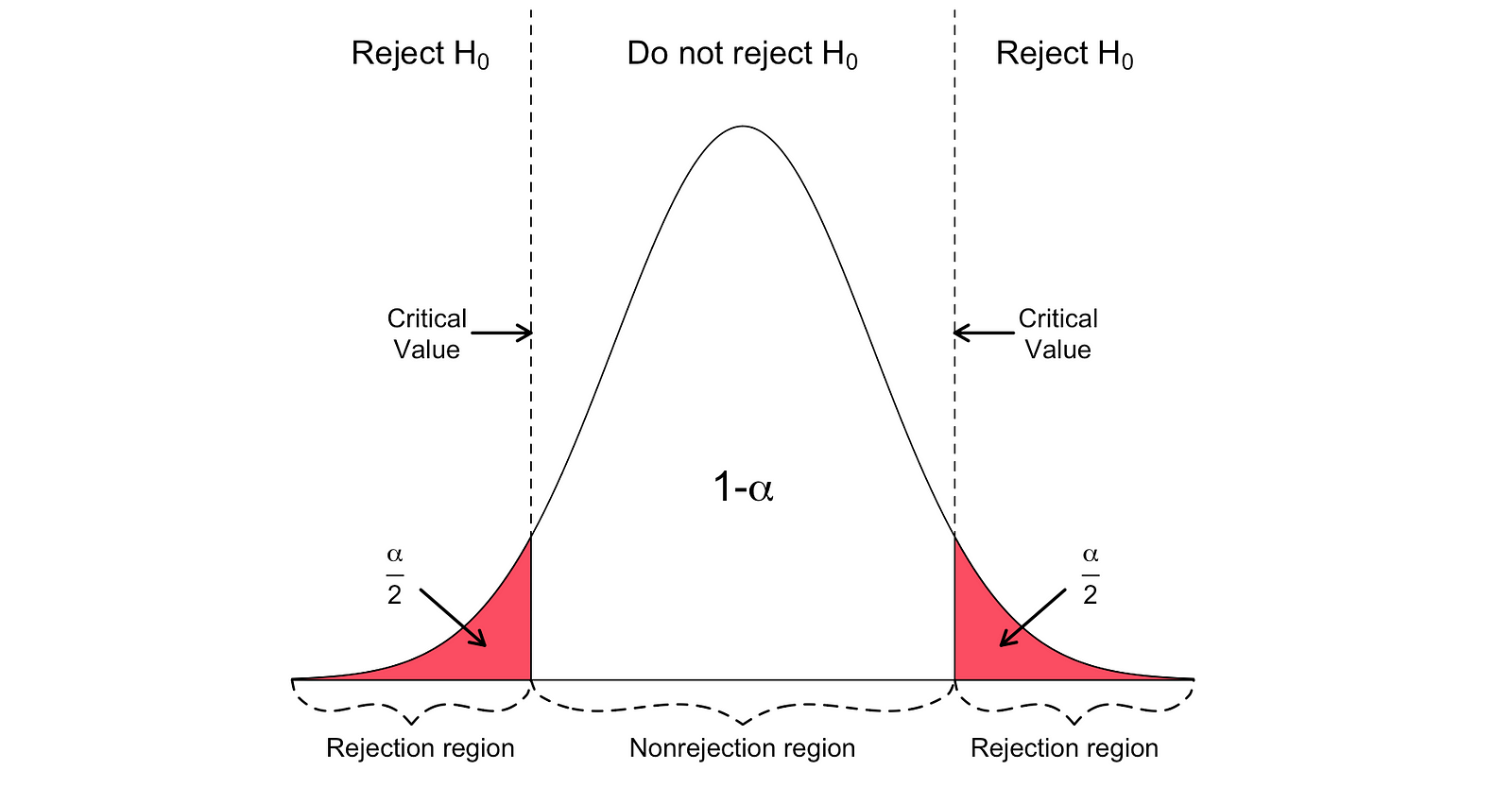

Statistical Hypothesis Testing

Testing a speculation in Statistics is a solution to check the outcomes of an experiment or survey to find out how significant they the outcomes are.

Basically, you are testing whether or not the obtained outcomes are legitimate by determining the chances that the outcomes have occurred by likelihood. If it’s the letter, then the outcomes will not be dependable and neither is the experiment. Hypothesis Testing is a part of the Statistical Inference.

Null and Alternative Hypothesis

Firstly, that you must decide the thesis you want to check. Then that you must formulate the Null Hypothesis and the Alternative Hypothesis. The check can have two attainable outcomes. Based on the statistical outcomes, you’ll be able to both reject the said speculation or settle for it.

As a rule of thumb, statisticians are likely to put the model or formulation of the speculation below the Null Hypothesis that must be rejected, whereas the appropriate and desired model is said below the Alternative Hypothesis.

Statistical Significance

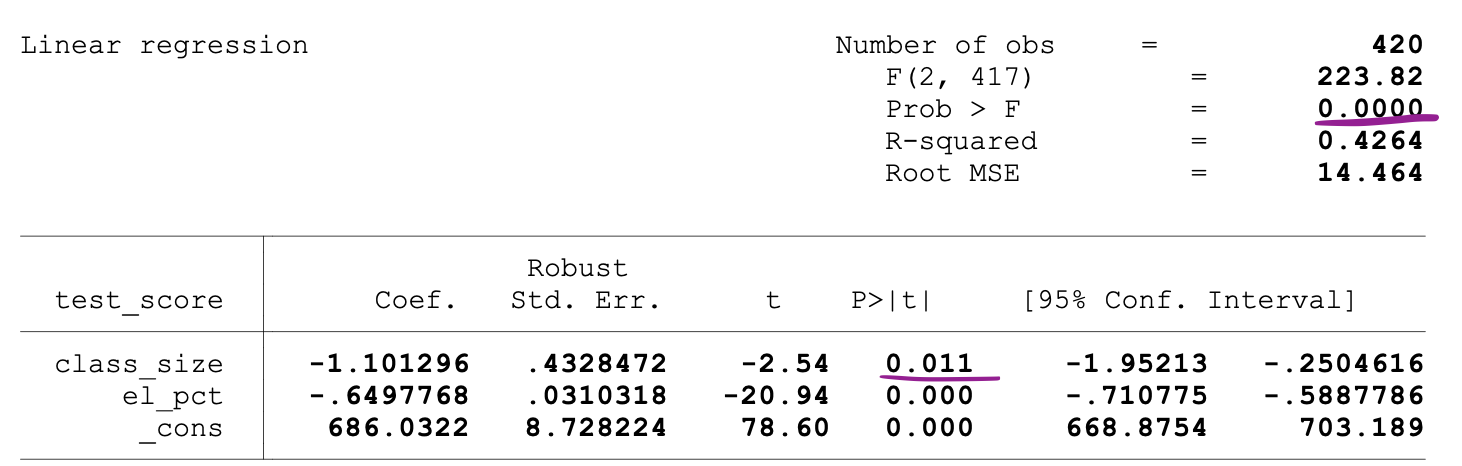

Let’s have a look at the sooner talked about instance the place we used the Linear Regression mannequin to research whether or not a penguin’s Flipper Length, the unbiased variable, has an affect on Body Mass, the dependent variable.

We can formulate this mannequin with the next statistical expression:

$$Y_{textual content{BodyMass}} = beta_0 + beta_1X_{textual content{FlipperLength}} + u_i

$$

Then, as soon as the OLS estimates of the coefficients are estimated, we will formulate the next Null and Alternative Hypothesis to check whether or not the Flipper Length has a statistically important affect on the Body Mass:

the place H0 and H1 symbolize Null Hypothesis and Alternative Hypothesis, respectively.

Rejecting the Null Hypothesis would imply {that a} one-unit enhance in Flipper Length has a direct affect on the Body Mass (on condition that the parameter estimate of β1 is describing this affect of the unbiased variable, Flipper Length, on the dependent variable, Body Mass). We can reformulate this speculation as follows:

$$start{circumstances}

H_0: hat{beta}_1 = 0

H_1: hat{beta}_1 neq 0

finish{circumstances}

$$

the place H0 states that the parameter estimate of β1 is the same as 0, that’s Flipper Length impact on Body Mass is statistically insignificant whereas H1 states that the parameter estimate of β1 is just not equal to 0, suggesting that Flipper Length impact on Body Mass is statistically important.

Type I and Type II Errors

When performing Statistical Hypothesis Testing, that you must think about two conceptual forms of errors: Type I error and Type II error.

Type I errors happen when the Null is incorrectly rejected, and Type II errors happen when the Null Hypothesis is incorrectly not rejected. A confusion matrix may also help you clearly visualize the severity of those two forms of errors.

As a rule of thumb, statisticians are likely to put the model of the speculation below the Null Hypothesis that that must be rejected, whereas the appropriate and desired model is said below the Alternative Hypothesis.

Statistical Tests

Once the you’ve got stataed the Null and the Alternative Hypotheses and outlined the check assumptions, the following step is to find out which statistical check is acceptable and to calculate the check statistic.

Whether or to not reject or not reject the Null may be decided by evaluating the check statistic with the crucial worth. This comparability exhibits whether or not or not the noticed check statistic is extra excessive than the outlined crucial worth.

It can have two attainable outcomes:

- The check statistic is extra excessive than the crucial worth → the null speculation may be rejected

- The check statistic is just not as excessive because the crucial worth → the null speculation can’t be rejected

The crucial worth relies on a pre-specified significance degree α (often chosen to be equal to five%) and the kind of likelihood distribution the check statistic follows.

The crucial worth divides the realm below this likelihood distribution curve into the rejection area(s) and non-rejection area. There are quite a few statistical checks used to check numerous hypotheses. Examples of Statistical checks are Student’s t-test, F-test, Chi-squared check, Durbin-Hausman-Wu Endogeneity check, White Heteroskedasticity check. In this handbook, we’ll have a look at two of those statistical checks: the Student’s t-test and the F-test.

Student’s t-test

One of the best and hottest statistical checks is the Student’s t-test. You can use it to check numerous hypotheses, particularly when coping with a speculation the place the primary space of curiosity is to search out proof for the statistically important impact of a single variable.

The check statistics of the t-test follows Student’s t distribution and may be decided as follows:

$$T_{textual content{stat}} = frac{hat{beta}_i – h_0}{SE(hat{beta})}

$$

the place h0 within the nominator is the worth towards which the parameter estimate is being examined. So, the t-test statistics are equal to the parameter estimate minus the hypothesized worth divided by the usual error of the coefficient estimate.

Let’s use this for our earlier speculation, the place we wished to check whether or not Flipper Length has a statistically important affect on Body Mass or not. This check may be carried out utilizing a t-test. The h0 is in that case equal to the 0 because the slope coefficient estimate is examined towards a price of 0.

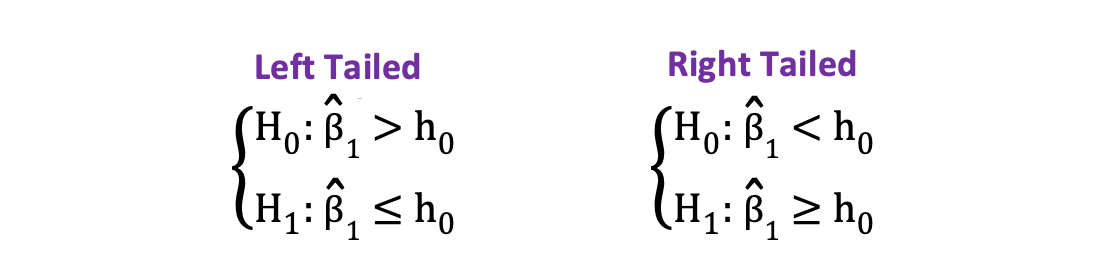

Two-sided vs one-sided t-test

There are two variations of the t-test: a two-sided t-test and a one-sided t-test. Whether you want the previous or the latter model of the check relies upon completely on the speculation that you simply need to check.

You can use the two-sided or two-tailed t-test when the speculation is testing equal versus not equal relationship below the Null and Alternative Hypotheses. It could be much like the next instance:

$$H_{0} = beta_hat_1 = h_0

H_{1} = beta_hat_1 neq h_0$$

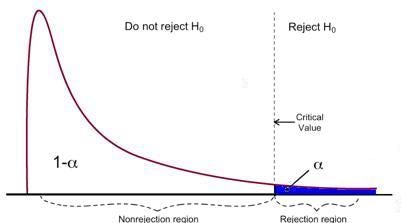

The two-sided t-test has two rejection areas as visualized within the determine beneath:

In this model of the t-test, the Null is rejected if the calculated t-statistics is both too small or too giant.

$$T_{textual content{stat}} < -t_{alpha,N} textual content{ or } T_{textual content{stat}} > t_{alpha,N}

$$

$$|T_{textual content{stat}}| > t_{alpha,N}

$$

Here, the check statistics are in comparison with the crucial values based mostly on the pattern dimension and the chosen significance degree. To decide the precise worth of the cutoff level, you should utilize a two-sided t-distribution desk.

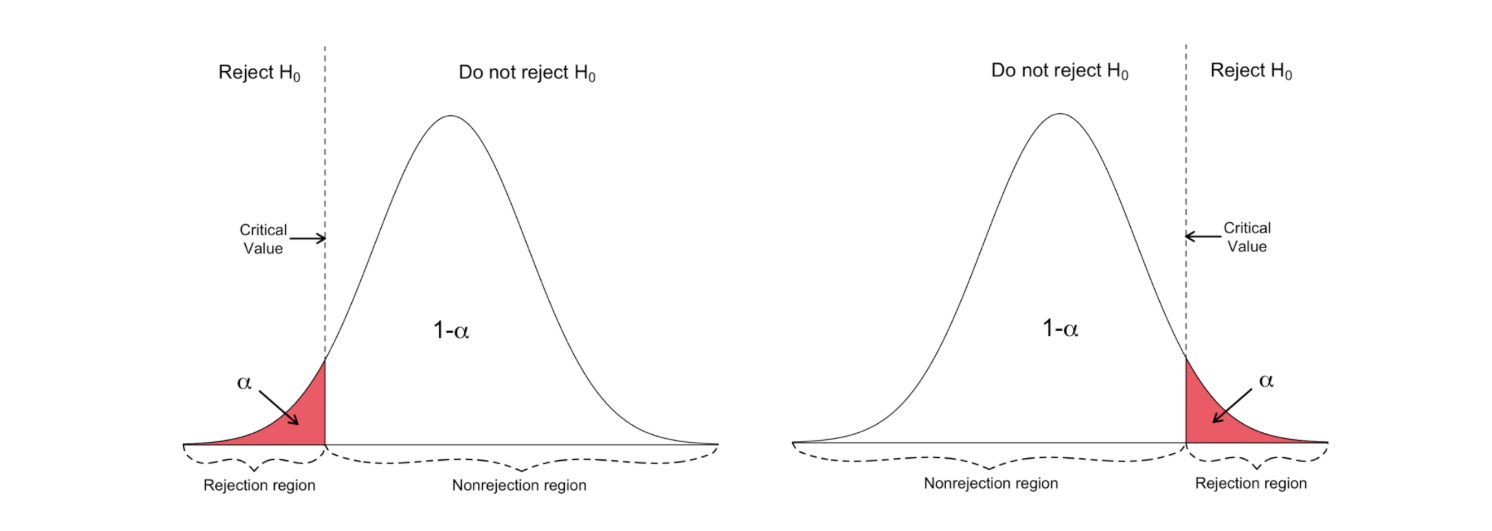

On the opposite hand, you should utilize the one-sided or one-tailed t-test when the speculation is testing constructive/adverse versus adverse/constructive relationships below the Null and Alternative Hypotheses. It appears to be like like this:

One-sided t-test has a single rejection area. Depending on the speculation facet, the rejection area is both on the left-hand facet or the right-hand facet as visualized within the determine beneath:

In this model of the t-test, the Null is rejected if the calculated t-statistics is smaller/bigger than the crucial worth.

F-test

F-test is one other very talked-about statistical check typically used to check hypotheses testing a joint statistical significance of a number of variables. This is the case if you need to check whether or not a number of unbiased variables have a statistically important affect on a dependent variable.

Following is an instance of a statistical speculation that you may check utilizing the F-test:

$$start{circumstances}

H_0: hat{beta}_1 = hat{beta}_2 = hat{beta}_3 = 0

H_1: hat{beta}_1 neq hat{beta}_2 neq hat{beta}_3 neq 0

finish{circumstances}$$

the place the Null states that the three variables corresponding to those coefficients are collectively statistically insignificant, and the Alternative states that these three variables are collectively statistically important.

The check statistics of the F-test follows F distribution and may be decided as follows:

$$F_{textual content{stat}} = frac{(SSR_{textual content{restricted}} – SSR_{textual content{unrestricted}}) / q}{SSR_{textual content{unrestricted}} / (N – k_{textual content{unrestricted}} – 1)}

$$

the place :

- the SSRrestricted is the sum of squared residuals of the restricted mannequin, which is identical mannequin excluding from the info the goal variables said as insignificant below the Null

- the SSRunrestricted is the sum of squared residuals of the unrestricted mannequin, which is the mannequin that features all variables

- the q represents the variety of variables which can be being collectively examined for the insignificance below the Null

- N is the pattern dimension

- and the okay is the entire variety of variables within the unrestricted mannequin.

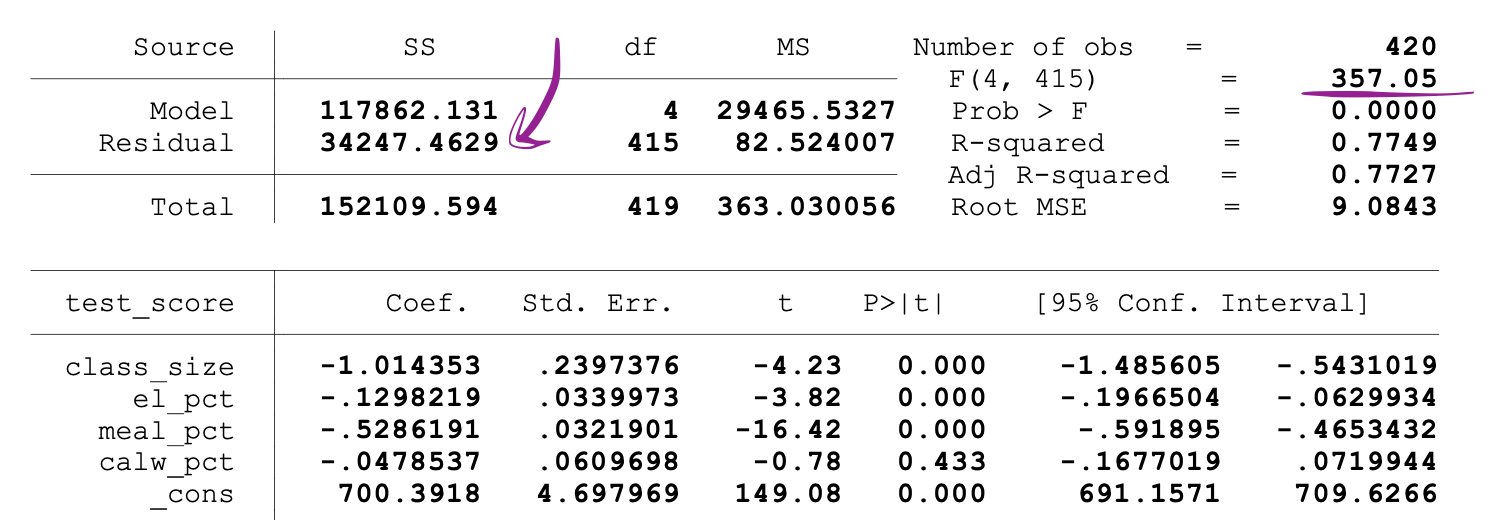

SSR values are supplied subsequent to the parameter estimates after operating the OLS regression, and the identical holds for the F-statistics as nicely.

Following is an instance of MLR mannequin output the place the SSR and F-statistics values are marked.

F-test has a single rejection area as visualized beneath:

If the calculated F-statistics is larger than the crucial worth, then the Null may be rejected. This means that the unbiased variables are collectively statistically important. The rejection rule may be expressed as follows:

$$F_{textual content{stat}} > F_{alpha,q,N}

$$

2-sample T-test

If you need to check whether or not there’s a statistically important distinction between the management and experimental teams’ metrics which can be within the type of averages (for instance, common buy quantity), metric follows student-t distribution. When the pattern dimension is smaller than 30, you should utilize 2-sample T-test to check the next speculation:

$$start{circumstances}

H_0: mu_{textual content{con}} = mu_{textual content{exp}}

H_1: mu_{textual content{con}} neq mu_{textual content{exp}}

finish{circumstances}$$

start{circumstances}$$

H_0: mu_{textual content{con}} – mu_{textual content{exp}} = 0

H_1: mu_{textual content{con}} – mu_{textual content{exp}} neq 0

finish{circumstances}

$$

the place the sampling distribution of technique of Control group follows Student-t distribution with levels of freedom N_con-1. Also, the sampling distribution of technique of the Experimental group additionally follows the Student-t distribution with levels of freedom N_exp-1.

Note that the N_con and N_exp are the variety of customers within the Control and Experimental teams, respectively.

$$hat{mu}_{textual content{con}} sim t(N_{textual content{con}} – 1)$$

hat{mu}_{textual content{exp}} sim t(N_{textual content{exp}} – 1)$$

$$

Then you’ll be able to calculate an estimate for the pooled variance of the 2 samples as follows:

$$S^2_{textual content{pooled}} = frac{(N_{textual content{con}} – 1) * sigma^2_{textual content{con}} + (N_{textual content{exp}} – 1) * sigma^2_{textual content{exp}}}{N_{textual content{con}} + N_{textual content{exp}} – 2} * left(frac{1}{N_{textual content{con}}} + frac{1}{N_{textual content{exp}}}proper)

$$

the place σ²_con and σ²_exp are the pattern variances of the Control and Experimental teams, respectively. Then the Standard Error is the same as the sq. root of the estimate of the pooled variance, and may be outlined as:

$$SE = sqrt{hat{S}^2_{textual content{pooled}}}

$$

Consequently, the check statistics of the 2-sample T-test with the speculation said earlier may be calculated as follows:

$$T = frac{hat{mu}_{textual content{con}} – hat{mu}_{textual content{exp}}}{sqrt{hat{S}^2_{textual content{pooled}}}}

$$

In order to check the statistical significance of the noticed distinction between pattern means, we have to calculate the p-value of our check statistics.

The p-value is the likelihood of observing values not less than as excessive because the frequent worth when this is because of a random likelihood. Stated in a different way, the p-value is the likelihood of acquiring an impact not less than as excessive because the one in your pattern knowledge, assuming the null speculation is true.

Then the p-value of the check statistics may be calculated as follows:

$$p_{textual content{worth}} = Pr[t leq -T text{ or } t geq T]$$

$$= 2 * Pr[t geq T]

$$

The interpretation of a p-value depends on the chosen significance degree, alpha, which you select earlier than operating the check through the energy evaluation.

If the calculated p-value seems to be smaller than equal to alpha (for instance, 0.05 for five% significance degree) we will reject the null speculation and state that there’s a statistically important distinction between the first metrics of the Control and Experimental teams.

Finally, to find out how correct the obtained outcomes are and likewise to remark in regards to the sensible significance of the obtained outcomes, you’ll be able to compute the Confidence Interval of your check through the use of the next system:

$$CI = left[ (hat{mu}_{text{con}} – hat{mu}_{text{exp}}) – t_{frac{alpha}{2}} * SE(hat{mu}_{text{con}} – hat{mu}_{text{exp}}), (hat{mu}_{text{con}} – hat{mu}_{text{exp}}) + t_{frac{alpha}{2}} * SE right]

$$

the place the t_(1-alpha/2) is the crucial worth of the check similar to the two-sided t-test with alpha significance degree. It may be discovered utilizing the t-table.

The Python code supplied performs a two-sample t-test, which is utilized in statistics to find out if two units of information are considerably completely different from one another. This explicit snippet simulates two teams (management and experimental) with knowledge following a t-distribution, calculates the imply and variance for every group, after which performs the next steps:

- It calculates the pooled variance, which is a weighted common of the variances of the 2 teams.

- It computes the usual error of the distinction between the 2 means.

- It calculates the t-statistic, which is the distinction between the 2 pattern means divided by the usual error. This statistic measures how a lot the teams differ in models of normal error.

- It determines the crucial t-value from the t-distribution for the given significance degree and levels of freedom, which is used to determine whether or not the t-statistic is giant sufficient to point a statistically important distinction between the teams.

- It calculates the p-value, which signifies the likelihood of observing such a distinction between means if the null speculation (that there is no such thing as a distinction) is true.

- It computes the margin of error and constructs the boldness interval across the distinction in means.

Finally, the code prints out the t-statistic, crucial t-value, p-value, and confidence interval. These outcomes can be utilized to deduce whether or not the noticed variations in means are statistically important or seemingly on account of random variation.

import numpy as np

from scipy.stats import t

N_con = 20

df_con = N_con - 1 # levels of freedom of Control

N_exp = 20

df_exp = N_exp - 1 # levels of freedom of Experimental

# Significance degree

alpha = 0.05

# knowledge of management group with t-distribution

X_con = np.random.standard_t(df_con,N_con)

# knowledge of experimental group with t-distribution

X_exp = np.random.standard_t(df_exp,N_exp)

# imply of management

mu_con = np.imply(X_con)

# imply of experimental

mu_exp = np.imply(X_exp)

# variance of management

sigma_sqr_con = np.var(X_con)

#variance of management

sigma_sqr_exp = np.var(X_exp)

# pooled variance

pooled_variance_t_test = ((N_con-1)*sigma_sqr_con + (N_exp -1) * sigma_sqr_exp)/(N_con + N_exp-2)*(1/N_con + 1/N_exp)

# Standard Error

SE = np.sqrt(pooled_variance_t_test)

# Test Statistics

T = (mu_con-mu_exp)/SE

# Critical worth for 2 sided 2 pattern t-test

t_crit = t.ppf(1-alpha/2, N_con + N_exp - 2)

# P-value of the 2 sided T-test utilizing t-distribution and its symmetric property

p_value = t.sf(T, N_con + N_exp - 2)*2

# Margin of Error

margin_error = t_crit * SE

# Confidence Interval

CI = [(mu_con-mu_exp) - margin_error, (mu_con-mu_exp) + margin_error]

print("T-score: ", T)

print("T-critical: ", t_crit)

print("P_value: ", p_value)

print("Confidence Interval of two pattern T-test: ", np.spherical(CI,2))2-sample Z-test

There are numerous conditions when it’s possible you’ll need to use a 2-sample z-test:

- if you wish to check whether or not there’s a statistically important distinction between the management and experimental teams’ metrics which can be within the type of averages (for instance, common buy quantity) or proportions (for instance, Click Through Rate)

- if the metric follows Normal distribution

- when the pattern dimension is bigger than 30, such that you should utilize the Central Limit Theorem (CLT) to state that the sampling distributions of the Control and Experimental teams are asymptotically Normal

Here we’ll make a distinction between two circumstances: the place the first metric is within the type of proportions (like Click Through Rate) and the place the first metric is within the type of averages (like common buy quantity).

Case 1: Z-test for evaluating proportions (2-sided)

If you need to check whether or not there’s a statistically important distinction between the Control and Experimental teams’ metrics which can be within the type of proportions (like CTR) and if the press occasion happens independently, you should utilize a 2-sample Z-test to check the next speculation:

$$start{circumstances}

H_0: p_{textual content{con}} = p_{textual content{exp}}

H_1: p_{textual content{con}} neq p_{textual content{exp}}

finish{circumstances}$$

$$start{circumstances}

H_0: p_{textual content{con}} – p_{textual content{exp}} = 0

H_1: p_{textual content{con}} – p_{textual content{exp}} neq 0

finish{circumstances}$$

the place every click on occasion may be described by a random variable that may take two attainable values: 1 (success) and 0 (failure). It additionally follows a Bernoulli distribution (click on: success and no click on: failure) the place p_con and p_exp are the chances of clicking (likelihood of success) of Control and Experimental teams, respectively.

So, after accumulating the interplay knowledge of the Control and Experimental customers, you’ll be able to calculate the estimates of those two chances as follows:

$$SE = sqrt{hat{S}^2_{textual content{pooled}}}

$$

$$Z = frac{(hat{p}_{textual content{con}} – hat{p}_{textual content{exp}})}{SE}

$$

Since we’re testing for the distinction in these chances, we have to get hold of an estimate for the pooled likelihood of success and an estimate for pooled variance, which may be achieved as follows:

$$hat{p}_{textual content{pooled}} = frac{X_{textual content{con}} + X_{textual content{exp}}}{N_{textual content{con}} + N_{textual content{exp}}} = frac{#textual content{clicks}_{textual content{con}} + #textual content{clicks}_{textual content{exp}}}{#textual content{impressions}_{textual content{con}} + #textual content{impressions}_{textual content{exp}}}

$$$$hat{S}^2_{textual content{pooled}} = hat{p}_{textual content{pooled}}(1 – hat{p}_{textual content{pooled}}) * left(frac{1}{N_{textual content{con}}} + frac{1}{N_{textual content{exp}}}proper)

$$

Then the Standard Error is the same as the sq. root of the estimate of the pooled variance. It may be outlined as:

$$SE = sqrt{hat{S}^2_{textual content{pooled}}}

$$

And so, the check statistics of the 2-sample Z-test for the distinction in proportions may be calculated as follows:

$$Z = frac{(hat{p}_{textual content{con}} – hat{p}_{textual content{exp}})}{SE}

$$

Then the p-value of this check statistics may be calculated as follows:

$$p_{textual content{worth}} = Pr[Z leq -T text{ or } z geq T]$$

$$= 2 * Pr[Z geq T]

$$

Finally, you’ll be able to compute the Confidence Interval of the check as follows:

$$CI = left[ (hat{p}_{text{con}} – hat{p}_{text{exp}}) – z_{frac{alpha}{2}} * SE, (hat{p}_{text{con}} – hat{p}_{text{exp}}) + z_{frac{alpha}{2}} * SE right]

$$

the place the z_(1-alpha/2) is the crucial worth of the check similar to the two-sided Z-test with alpha significance degree. You can discover it utilizing the Z-table.

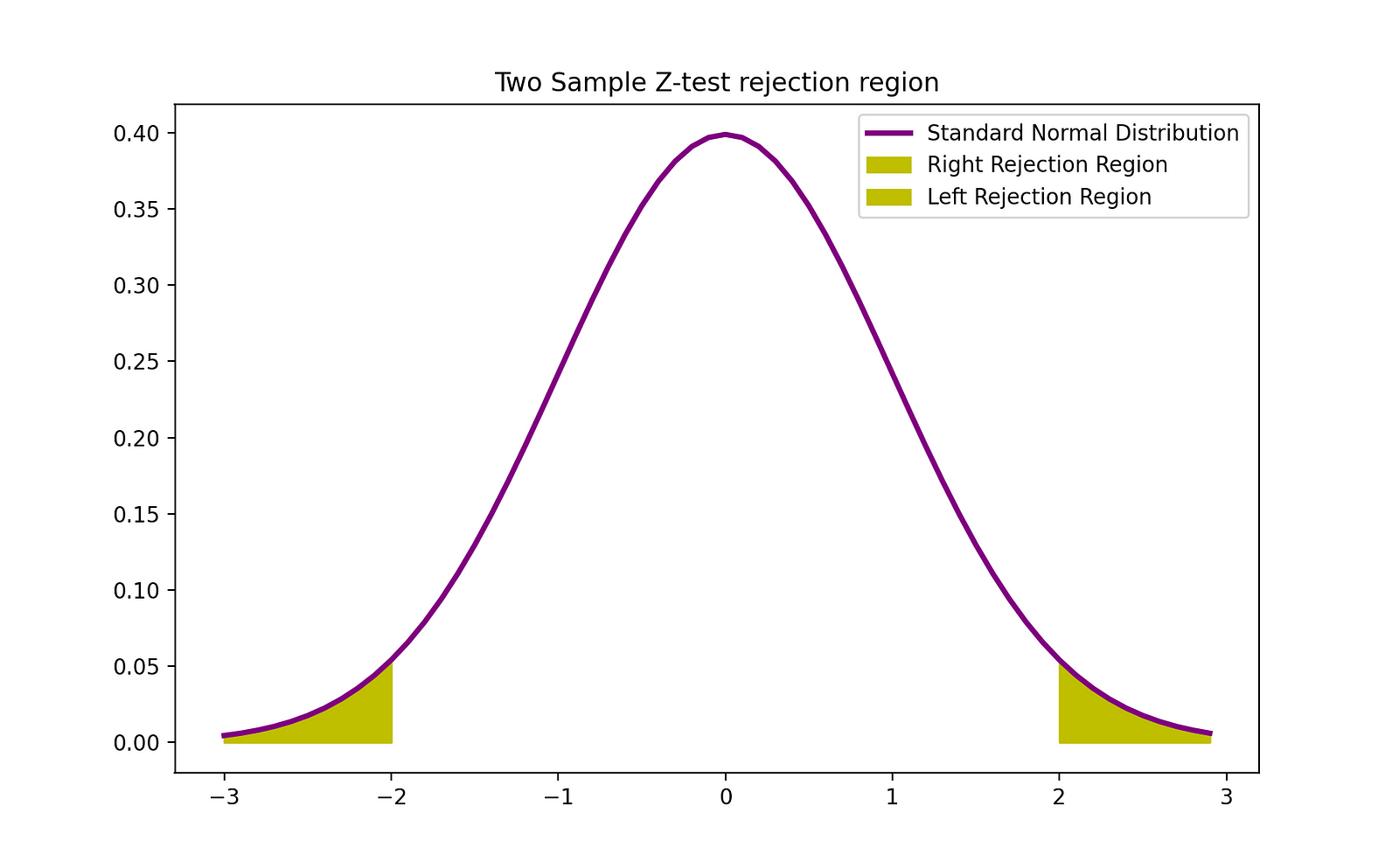

The rejection area of this two-sided 2-sample Z-test may be visualized by the next graph:

The Python code snippet you’ve supplied performs a two-sample Z-test for proportions. This sort of check is used to find out whether or not there’s a important distinction between the proportions of two teams. Here’s a quick rationalization of the steps the code performs:

- Calculates the pattern proportions for each the management and experimental teams.

- Computes the pooled pattern proportion, which is an estimate of the proportion assuming the null speculation (that there is no such thing as a distinction between the group proportions) is true.

- Calculates the pooled pattern variance based mostly on the pooled proportion and the sizes of the 2 samples.

- Derives the usual error of the distinction in pattern proportions.

- Calculates the Z-test statistic, which measures the variety of customary errors between the pattern proportion distinction and the null speculation.

- Finds the crucial Z-value from the usual regular distribution for the given significance degree.

- Computes the p-value to evaluate the proof towards the null speculation.

- Calculates the margin of error and the boldness interval for the distinction in proportions.

- Outputs the check statistic, crucial worth, p-value, and confidence interval, and based mostly on the check statistic and significant worth, it might print a press release to both reject or not reject the null speculation.

The latter a part of the code makes use of Matplotlib to create a visualization of the usual regular distribution and the rejection areas for the two-sided Z-test. This visible support helps to grasp the place the check statistic falls in relation to the distribution and the crucial values.

import numpy as np

from scipy.stats import norm

X_con = 1242 #clicks management

N_con = 9886 #impressions management

X_exp = 974 #clicks experimental

N_exp = 10072 #impressions experimetal

# Significance Level

alpha = 0.05

p_con_hat = X_con / N_con

p_exp_hat = X_exp / N_exp

p_pooled_hat = (X_con + X_exp)/(N_con + N_exp)

pooled_variance = p_pooled_hat*(1-p_pooled_hat) * (1/N_con + 1/N_exp)

# Standard Error

SE = np.sqrt(pooled_variance)

# check statsitics

Test_stat = (p_con_hat - p_exp_hat)/SE

# crucial worth usig the usual regular distribution

Z_crit = norm.ppf(1-alpha/2)

# Margin of error

m = SE * Z_crit

# two sided check and utilizing symmetry property of Normal distibution so we a number of with 2

p_value = norm.sf(Test_stat)*2

# Confidence Interval

CI = [(p_con_hat-p_exp_hat) - SE * Z_crit, (p_con_hat-p_exp_hat) + SE * Z_crit]

if np.abs(Test_stat) >= Z_crit:

print("reject the null")

print(p_value)

print("Test Statistics stat: ", Test_stat)

print("Z-critical: ", Z_crit)

print("P_value: ", p_value)

print("Confidence Interval of two pattern Z-test for proportions: ", np.spherical(CI,2))

import matplotlib.pyplot as plt

z = np.arange(-3,3, 0.1)

plt.plot(z, norm.pdf(z), label="Standard Normal Distribution",coloration="purple",linewidth = 2.5)

plt.fill_between(z[z>Z_crit], norm.pdf(z[z>Z_crit]), label="Right Rejection Region",coloration="y" )

plt.fill_between(z[z<(-1)*Z_crit], norm.pdf(z[z<(-1)*Z_crit]), label="Left Rejection Region",coloration="y" )

plt.title("Two Sample Z-test rejection area")

plt.legend()

plt.present()Case 2: Z-test for Comparing Means (2-sided)

If you need to check whether or not there’s a statistically important distinction between the Control and Experimental teams’ metrics which can be within the type of averages (like common buy quantity) you should utilize a 2-sample Z-test to check the next speculation:

$$start{circumstances}

H_0: {CR}_{textual content{con}} = {CR}_{textual content{exp}}

H_1:{CR}_{textual content{con}} neq {CR}_{textual content{exp}}

finish{circumstances}$$

$$start{circumstances}

H_0: {CR}_{textual content{con}} – {CR}_{textual content{exp}} = 0

H_1: {CR}_{textual content{con}} – {CR}_{textual content{exp}} neq 0

finish{circumstances}$$

the place the sampling distribution of technique of the Control group follows Normal distribution with imply mu_con and σ²_con/N_con. Moreover, the sampling distribution of technique of the Experimental group additionally follows the Normal distribution with imply mu_exp and σ²_exp/N_exp.

$$hat{mu}_{textual content{con}} sim N(mu_{con}, frac{sigma^2_{con}}{N_{con}})$$

$$hat{mu}_{textual content{exp}} sim N(mu_{exp}, frac{sigma^_{exp}2}{N_{exp}})$$

$$

Then the distinction within the technique of the management and experimental teams additionally follows Normal distributions with imply mu_con-mu_exp and variance σ²_con/N_con + σ²_exp/N_exp.

$$hat{mu}_{textual content{con}}-hat{mu}_{textual content{exp}} sim N(mu_{con}-mu_{exp}, frac{sigma^2_{con}}{N_{con}}+frac{sigma^2_{exp}}{N_{exp}})$$

Consequently, the check statistics of the 2-sample Z-test for the distinction in means may be calculated as follows:

$$T = frac{hat{mu}_{textual content{con}}-hat{mu}_{textual content{exp}}}{sqrt{frac{sigma^2_{con}}{N_{con}} + frac{sigma^2_{exp}}{N_{exp}}}} sim N(0,1)$$

The Standard Error is the same as the sq. root of the estimate of the pooled variance and may be outlined as:

$$SE = sqrt{frac{sigma^2_{con}}{N_{con}} + frac{sigma^2_{exp}}{N_{exp}}}}$$

Then the p-value of this check statistics may be calculated as follows:

$$p_{textual content{worth}} = Pr[Z leq -T text{ or } Z geq T]$$

$$= 2 * Pr[Z geq T]

$$

Finally, you’ll be able to compute the Confidence Interval of the check as follows:

$$CI = [(mu_hat_{con} – mu_hat_{exp}) – z_{1-alpha/2}*SE,((mu_hat_{con} – mu_hat_{exp}) + z_{1-alpha/2)*SE]$$

The Python code supplied seems to be arrange for conducting a two-sample Z-test, usually used to find out if there’s a important distinction between the technique of two unbiased teams. In this context, the code may be evaluating two completely different processes or remedies.

- It generates two arrays of random integers to symbolize knowledge for a management group (

X_A) and an experimental group (X_B). - It calculates the pattern means (

mu_con,mu_exp) and variances (variance_con,variance_exp) for each teams. - The pooled variance is computed, which is used within the denominator of the check statistic system for the Z-test, offering a measure of the info’s frequent variance.

- The Z-test statistic (

T) is calculated by taking the distinction between the 2 pattern means and dividing it by the usual error of the distinction. - The p-value is calculated to check the speculation of whether or not the technique of the 2 teams are statistically completely different from one another.

- The crucial Z-value (

Z_crit) is decided from the usual regular distribution, which defines the cutoff factors for significance. - A margin of error is computed, and a confidence interval for the distinction in means is constructed.

- The check statistic, crucial worth, p-value, and confidence interval are printed to the console.

Lastly, the code makes use of Matplotlib to plot the usual regular distribution and spotlight the rejection areas for the Z-test. This visualization may also help in understanding the results of the Z-test when it comes to the place the check statistic lies relative to the distribution and the crucial values for a two-sided check.

import numpy as np

from scipy.stats import norm

N_con = 60

N_exp = 60

# Significance Level

alpha = 0.05

X_A = np.random.randint(100, dimension = N_con)

X_B = np.random.randint(100, dimension = N_exp)

# Calculating technique of management and experimental teams

mu_con = np.imply(X_A)

mu_exp = np.imply(X_B)

variance_con = np.var(X_A)

variance_exp = np.var(X_B)

# Pooled Variance

pooled_variance = np.sqrt(variance_con/N_con + variance_exp/N_exp)

# Test statistics

T = (mu_con-mu_exp)/np.sqrt(variance_con/N_con + variance_exp/N_exp)

# two sided check and utilizing symmetry property of Normal distibution so we a number of with 2

p_value = norm.sf(T)*2

# Z-critical worth

Z_crit = norm.ppf(1-alpha/2)

# Margin of error

m = Z_crit*pooled_variance

# Confidence Interval

CI = [(mu_con - mu_exp) - m, (mu_con - mu_exp) + m]

print("Test Statistics stat: ", T)

print("Z-critical: ", Z_crit)

print("P_value: ", p_value)

print("Confidence Interval of two pattern Z-test for proportions: ", np.spherical(CI,2))

import matplotlib.pyplot as plt

z = np.arange(-3,3, 0.1)

plt.plot(z, norm.pdf(z), label="Standard Normal Distribution",coloration="purple",linewidth = 2.5)

plt.fill_between(z[z>Z_crit], norm.pdf(z[z>Z_crit]), label="Right Rejection Region",coloration="y" )

plt.fill_between(z[z<(-1)*Z_crit], norm.pdf(z[z<(-1)*Z_crit]), label="Left Rejection Region",coloration="y" )

plt.title("Two Sample Z-test rejection area")

plt.legend()

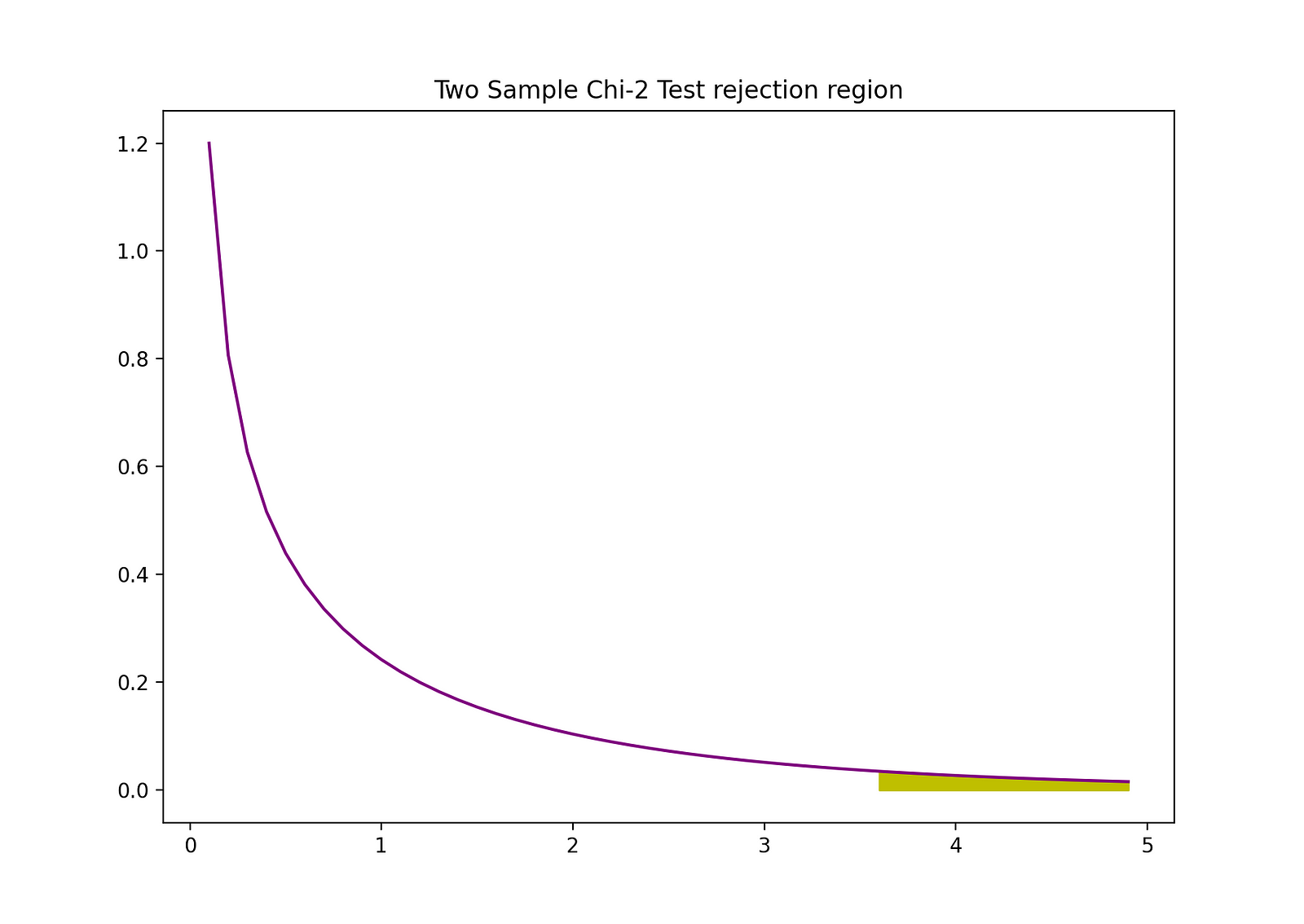

plt.present()Chi-Squared check

If you need to check whether or not there’s a statistically important distinction between the Control and Experimental teams’ efficiency metrics (for instance their conversions) and also you don’t actually need to know the character of this relationship (which one is best) you should utilize a Chi-Squared check to check the next speculation:

$$start{circumstances}

H_0: CR_{textual content{con}} = CR_{textual content{exp}}

H_1: CR_{textual content{con}} neq CR_{textual content{exp}}

finish{circumstances}$$

$$start{circumstances}

H_0: CR_{textual content{con}} – CR_{textual content{exp}} = 0

H_1: CR_{textual content{con}} – CR_{textual content{exp}} neq 0

finish{circumstances}

$$

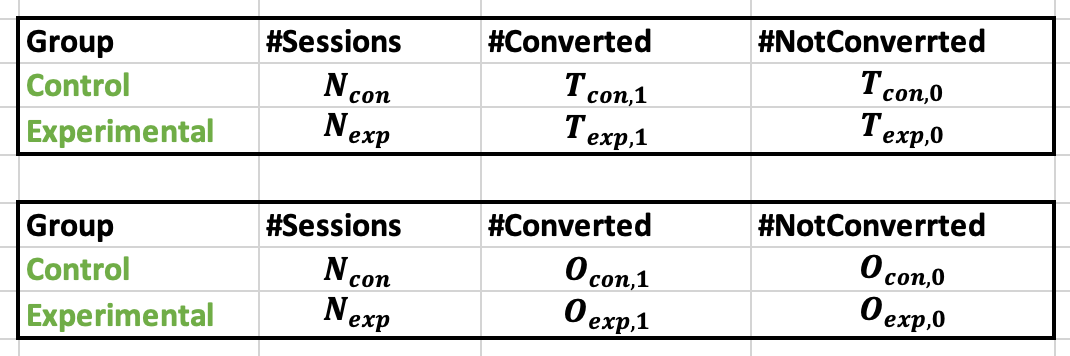

Note that the metric needs to be within the type of a binary variable (for instance, conversion or no conversion/click on or no click on). The knowledge can then be represented within the type of the next desk, the place O and T correspond to noticed and theoretical values, respectively.

Then the check statistics of the Chi-2 check may be expressed as follows:

$$T = sum_{i} frac{(Observed_i – Expected_i)^2}{Expected_i}$$

the place the Observed corresponds to the noticed knowledge and the Expected corresponds to the theoretical worth, and that i can take values 0 (no conversion) and 1(conversion). It’s vital to see that every of those elements has a separate denominator. The system for the check statistics when you could have two teams solely may be represented as follows:

$$T = frac{(Observed_{con,1} – T_{con,1})^2}{T_{con,1}} + frac{(Observed_{con,0} – T_{con,0})^2}{T_{con,0}} + frac{(Observed_{exp,1} – T_{exp,1})^2}{T_{exp,1}} + frac{(Observed_{exp,0} – T_{exp,0})^2}{T_{exp,0}} $$

The anticipated worth is just equal to the variety of instances every model of the product is considered multiplied by the likelihood of it resulting in conversion (or to a click on in case of CTR).

Note that, because the Chi-2 check is just not a parametric check, its Standard Error and Confidence Interval can’t be calculated in a normal manner as we did within the parametric Z-test or T-test.

The rejection area of this two-sided 2-sample Z-test may be visualized by the next graph:

The Python code you’ve got shared is for conducting a Chi-squared check, a statistical speculation check that’s used to find out whether or not there’s a important distinction between the anticipated frequencies and the noticed frequencies in a number of classes.

In the supplied code snippet, it appears to be like just like the check is getting used to match two categorical datasets:

- It calculates the Chi-squared check statistic by summing the squared distinction between noticed (

O) and anticipated (T) frequencies, divided by the anticipated frequencies for every class. This is named the squared relative distance and is used because the check statistic for the Chi-squared check. - It then calculates the p-value for this check statistic utilizing the levels of freedom, which on this case is assumed to be 1 (however this might usually depend upon the variety of classes minus one).

- The Matplotlib library is used to plot the likelihood density operate (pdf) of the Chi-squared distribution with one diploma of freedom. It additionally highlights the rejection area for the check, which corresponds to the crucial worth of the Chi-squared distribution that the check statistic should exceed for the distinction to be thought-about statistically important.

The visualization helps to grasp the Chi-squared check by exhibiting the place the check statistic lies in relation to the Chi-squared distribution and its crucial worth. If the check statistic is throughout the rejection area, the null speculation of no distinction in frequencies may be rejected.

import numpy as np

from scipy.stats import chi2

O = np.array([86, 83, 5810,3920])

T = np.array([105,65,5781, 3841])

# Squared_relative_distance

def calculate_D(O,T):

D_sum = 0

for i in vary(len(O)):

D_sum += (O[i] - T[i])**2/T[i]

return(D_sum)

D = calculate_D(O,T)

p_value = chi2.sf(D, df = 1)

import matplotlib.pyplot as plt

# Step 1: decide a x-axis vary like in case of z-test (-3,3,0.1)

d = np.arange(0,5,0.1)

# Step 2: drawing the preliminary pdf of chi-2 with df = 1 and x-axis d vary we simply created

plt.plot(d, chi2.pdf(d, df = 1), coloration = "purple")

# Step 3: filling within the rejection area

plt.fill_between(d[d>D], chi2.pdf(d[d>D], df = 1), coloration = "y")

# Step 4: including title

plt.title("Two Sample Chi-2 Test rejection area")

# Step 5: exhibiting the plt graph

plt.present()P-Values

Another fast solution to decide whether or not to reject or to help the Null Hypothesis is through the use of p-values. The p-value is the likelihood of the situation below the Null occurring. Stated in a different way, the p-value is the likelihood, assuming the null speculation is true, of observing a consequence not less than as excessive because the check statistic. The smaller the p-value, the stronger is the proof towards the Null Hypothesis, suggesting that it may be rejected.

The interpretation of a p-value depends on the chosen significance degree. Most typically, 1%, 5%, or 10% significance ranges are used to interpret the p-value. So, as an alternative of utilizing the t-test and the F-test, p-values of those check statistics can be utilized to check the identical hypotheses.